LIC has been Indians’ security net for decades. It is now facing an uncertain future

LIC has been Indians’ security net for decades. It is now facing an uncertain future

Every so often, India’s largest and oldest insurer, a staid socialist-era state-run firm, sheds its Clark Kent-image to swoop in and save other distressed government companies. That’s because the Life Insurance Corporation of India, commonly known as LIC, is also one of the most profitable of all such firms, accruing Rs 48,436 crore in the Financial Year 2018-’19 alone. In the first 10 months of the current financial year, it posted a profit of Rs 23,273 crore, up over 42% from the same period a year ago.

LIC isn’t immune to market vagaries, though. Certainly not in times of a terrible pandemic like this. Having led to the death of over 16,591 people globally – 11 in India – since its emergence in December 2019, Covid-19 has wreaked havoc on stock markets everywhere. India’s benchmark S&P BSE Sensex alone has lost around 37% of its market value over the past month. Nearly all of LIC’s investments have suffered bloody blows, losing Rs 1.84 lakh crore in 2020, according to an Economic Times report on March 23. Whether this haemorrhaging will scupper the government’s plans for an initial public offering for LIC remains to be seen. Managing Rs 30 lakh crore in assets, the behemoth’s market debut was expected to rake in Rs 70,000 crore, which would then go towards bridging India’s widening fiscal deficit.

That a state-run giant is still playing such a pivotal role, even three decades after the Indian economy’s unshackling, is a testimony to LIC’s pre-eminent position – the firm’s market share is bigger than the rest of the players in the Indian insurance industry put together. Now, contrast that to the hodgepodge origins of this Superman.

A new insurer

LIC was a product of Indian Prime Minister Jawaharlal Nehru’s vision. “The nationalisation of life insurance is an important step in our march towards a socialist society,” Nehru announced in Parliament in 1956 when the ordinance to nationalise insurance companies was passed. “Its objective will be to serve the individual as well as the state.”

This process of nationalisation was a mammoth exercise, amalgamating 154 Indian and 16 non-Indian insurers with 75 provident societies – all under the Life Insurance Corporation Act of 1956. Before this, insurance in the country was largely meant to cater to wealthy Indians and colonial businessmen. The first known insurance policy in India dates back to the early 19th century, according to the Insurance Regulatory Development Authority of India. The East India Company was still finding its roots in the subcontinent. To protect the interest of its European masters, Oriental Insurance Company was set up in Calcutta, now Kolkata, in 1818.

That company did not last long, though. Meanwhile, wealthy Indians, too, began to feel the need for insurance. By the second decade of the 20th century, there were several small and large insurance providers in India, prompting the British-Indian to introduce the Insurance Companies Act in 1912 to codify this business. This Act saw fresh iterations in 1928 and in 1938, by which time India had 176 insurance companies.

A newly-minted democracy by 1950, India felt the dire need to take stock of these companies, along with those selling provident fund products. Some of these were homegrown, others served foreign firms. It wasn’t until 1956, however, that the market was consolidated. Over the next 44 years, LIC, India’s sole life insurance provider, spread its presence across the nooks, corners, and gullies of the country, turning it into a middle-class obsession and a pillar of financial planning in the family. This process was spearheaded by the ubiquitous, friendly neighbourhood, and occasionally annoying, LIC agent.

Special agent

“Some days in March, I come home around 11 pm, after having driven across different parts of the city,” says Rajeev Sharma, a 58-year-old agent in New Delhi. Sharma has a day job with a civic infrastructure company. “But had it not been for this LIC agent work, I would’ve not been able to buy my own house or get my two kids married,” he says.

Sharma isn’t alone. As of March 2019, LIC had over 1.1 million insurance agents in India who earn commissions for each product sold. That is at least 100,000 more than all private insurers combined. Many middle-class Indian homes have dedicated LIC agents – distant relatives, affably pushy neighbours, long-term colleagues. “Sometimes, even if a family wants to try newer options, they take our advice first,” said KC Krishna Kumar, an agent since 1988 in Kozhikode in Kerala. “After all, many of us have been with these clients for decades,” he says, referring to the more than 800 customers he services today.

LIC has rewarded its high-performing agents handsomely, including bonuses and all-expenses-paid domestic and international holidays. In 2013, for instance, agents Bharat Parekh and Ravi Jethani earned Rs 4 crore and Rs 3 crore, respectively, as annual commissions, as reported by The Economic Times. At that time, the then LIC chairman, DK Mehrotra, earned Rs 87 lakh in annual salary, 1/4th of what Parekh made. “An LIC agent was looked down upon and the perception was that only those who had nothing else to do in life became LIC agents,” Parekh told The Economic Times. And yet, it was a profession that turned his life around. He called it “the world’s best profession.”

Yet, it was not about the agent alone. Indian families trusted the products, too. Besides being a tax-saving instrument, LIC’s long-term endowment policies are particularly popular as a retirement plan. Like a fixed deposit account in a nationalised bank, or a locker for their jewellery, the LIC policy is an unmistakable middle-class Indian symbol.

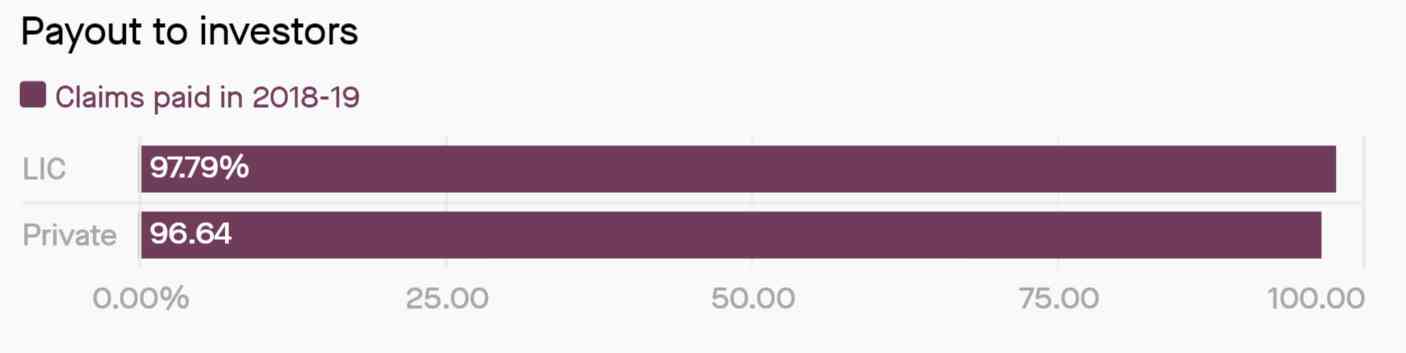

This trust factor has also remained high due to the consistency of clearing claims. Besides, LIC is also the only insurer that offers sovereign guarantee, ensuring that investments are completely secure. “When I started working in the 1980s, the LIC policy was my security blanket. Everyone I knew who could afford to pay premiums had a policy,” says Gurvinder Madan, a retired banker from Chandigarh.

However, will even this be enough in future? Even as its straddles two worlds – socialist roots and the country’s modern economy – how it adapts to change will matter a lot for LIC. Yet, it has been adapting since at least the early 1990s when India began shedding protectionism.

The continuing makeover

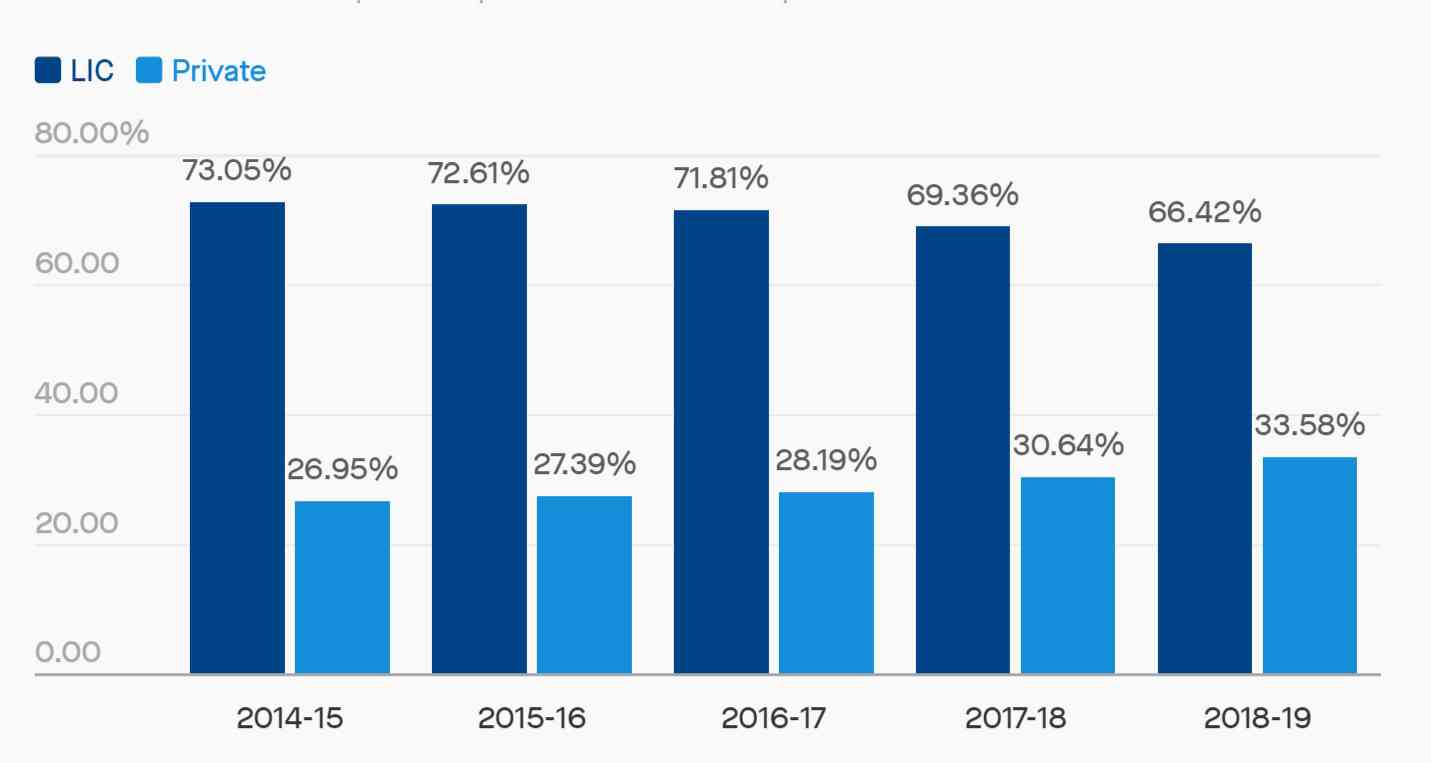

It was in 1993 that the Reserve Bank of India set up a committee to look at opening up the insurance sector to private players. In 1999. The government set up the Insurance Regulatory and Development Authority to look into reforming this industry. At the turn of the century, in 2000, India finally opened up the insurance sector to private companies, including foreign ones who could own up to 26% in Indian firms. It has been 20 years since, yet LIC has retained the largest piece of the pie.

LIC's market share compared to private insurance companies. Source: Insurance Regulatory and Development Authority via Quartz

Selling family silver

Given that LIC is a profit-making entity, unlike, say, national carrier Air India or the telco BSNL, divesting it seems counterintuitive to many. “The LIC [listing] could also raise significant questions as to why one would sell one of the biggest cash cows first, rather than looking to aggressively sell other public sector companies that have been bleeding financially for a long time,” says Abhijeet Ramachandrran, co-owner of Tips2trade, a Mumbai-based financial training organisation.

LIC will also be among the last of the financial sector entities to be listed on the stock market. This, according to experts, has held the insurer back from becoming a dynamic market player. And while LIC has a loyal customer base, it is being ridden with inefficiencies. A public listing could help fix that. “Once enterprises like LIC get listed, they would also be bound by the Securities and Exchange Board of India’s regulations which would automatically bring about discipline and curb lethargic behaviour or operational inefficiencies,” says Nirali Shah, a senior research analyst at Samco Securities, a Mumbai-based online stockbroker.

The news of listing, though, raises concerns. First, protesting murmurs already abound over the Narendra Modi government directing LIC’s financial muscle to save India’s non-performing assets crisis. For instance, LIC is one of the largest stakeholders in the troubled infrastructure lending company IL&FS.

“Investors in LIC’s insurance and other schemes are receiving lower rates of return because LIC is subsidising incompetence at best and malfeasance at worst in institutions such as IDBI Bank and IL&FS,” Jaimini Bhagwat, the RBI chair professor at Delhi-based think tank Indian Council for Research on International Economic Relations, wrote in Business Standard . “LIC’s foremost priority has to be providing efficient services and high returns to existing policyholders and to widen its reach. By contrast, the government is pushing LIC into taking unwarranted risks and [Insurance Regulatory and Development Authority] has been complicit.”

Others, however, believe LIC’s socialist origins have kept it on the path of doing right by investors. “LIC being a quasi-government organisation, it is clear it does not tend to carry out operations keeping profitability as its prime motive. In fact, such organisations cater to the much-needed social welfare which is considered for the greater good of Indian society,” says Shah of Samco Securities. That perception has stayed on with generations of customers. However, with the increasing availability of other savings tools and a more open market, this is changing, too.

Changing times

Indian millennials today are largely pushed into buying LIC’s policies by parents and other elders in their family – or by the never-say-die, avuncular LIC agent. “I didn’t want to be saddled with a Rs 50,000 annual policy, especially when I could invest that money in mutual funds,” says 28-year-old digital marketer Riddhima Arora of New Delhi.

Even for the children of LIC agents, such as 31-year-old Aniket Sharma, an insurance policy was too old school. “It’s a slow-moving investment and doesn’t grow my money as effectively. I would rather buy a term insurance for security, and invest in instruments that are more lucrative,” says the Noida-based corporate consultant. Yet, as she and the policy grew older, Arora began seeing value in LIC’s slow but sure gains. “I understand the benefits, but I don’t think anyone among my friends would actually buy the policy themselves,” she says.

In short, even though LIC may seem to have lost its cool quotient, its financial performance is intact. For how long, no one’s sure. After all, coronavirus is still ripping open gaping holes in the global economic system, and nobody knows when that will end. Can the super-PSU insure India, and Indians, against this pandemonium?

Source: Scroll.in