State-run Life Insurance Corporation of India (LIC) has been the main driver of life insurance industry premium accounting for about 69% of total first year premium collected in FY20, with the private sector accounting for the balance 31%. However, over the past decade, private life insurance players have continued to gain market share from LIC due to various measures and regulatory changes in the insurance sector, says a research note.

In the report, CARE Ratings says, "The declining market share of LIC as compared to private players, is further noticeable for the month of April 2020 as well, where LIC has lost share from 53.3% in April 2019 to a sharper decline to 44.4% in April 2020. Even as LIC has gained a 0.5% share in overall first year premium for April 2020, however, private companies have gained a 7% share in sum assured as private companies have sold a larger share of protection plans which have a higher sum assured as compared to traditional plans."

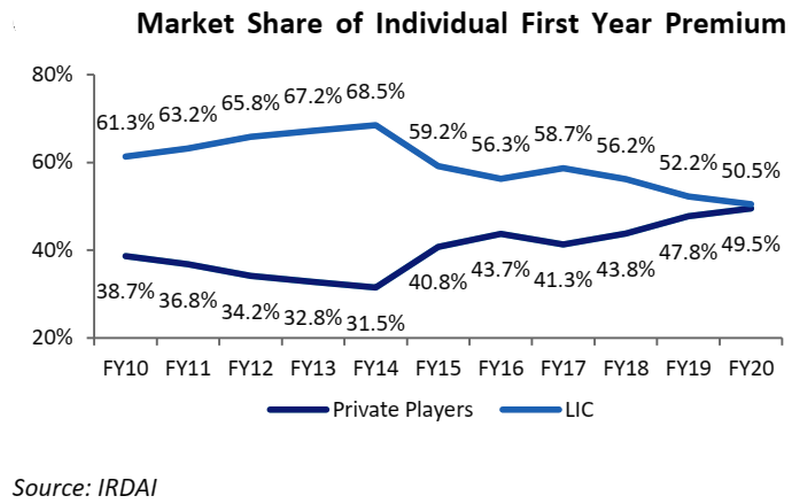

According to the ratings agency, individual single and non-single premium income continues to play a major role for LIC as they contributed 50.5% of total first year individual premium income in FY20 compared with 61.3% in FY10. In comparison, the contribution of individual single and non-single premium income in total first year individual premium income during FY20 was 49.5% for private insurance companies as against 38.7% recorded in FY10, as private players focused more on individual premium products.

"The rise of the private companies can be attributed to focus on metro cities, on high value insurance policies, which generated larger premiums, digital push, and expansion of multiple distribution channels like bancassurance and digital compared with LIC’s focus on the agency channel," the report says.

The overall life insurance industry in India recorded a first-year premium income of Rs2.6 lakh crore during FY20 as against Rs1.1 lakh crore during FY10, registering a compounded annual growth rate (CAGR) of 8.2% during FY10-FY20. While private sector insurers posted a CAGR of 7.0% growth (FY10- FY20) in their first-year premium income, LIC recorded 8.7% CAGR growth.

CARE Ratings has divided the 10-year period in two phases, first when private insurers face larger impact of regulatory changes and second in which private insurers recovered lost ground and outpaced LIC.

The first phase was four years between FY10 to FY14. On the basis of total individual first year premium income, the market share of LIC witnessed an increasing trend from FY10 to FY14, while private players witnessed a declining market share trend during the same period (see chart below).

"Bulk of the decline happened during the years of major regulatory changes, which necessitated significant effort on the part of the insurers to adapt. Several products (predominantly unit linked insurance policies-ULIPs) were rendered ineligible and insurers had to re-design them to comply with the new regulations, resulting in a sharp decline in product offerings," the ratings agency says.

The second phase is for six years between FY14 to FY20, which can be divided in to two further phases that highlight decline in first year premium collections of LIC. Since FY14 to FY17, LIC’s individual first year premium growth was slow (CAGR of 2.2%) as compared to private players CAGR of 13.7% as there was a rise in distribution channels of private players.

From FY17 to FY20, LIC’s individual first premium registered a CAGR growth of 3.0% as compared to CAGR growth of 11.9% in private players.

Since FY14 to FY20, LIC’s share consistently declined from 68.5% in FY14 to 50.5% in FY20. Whereas, the market share of private insurers has increased from 31.5% in FY14 to 49.5% in FY20.

The shift in individual first year premium market share from LIC to private players can be attributed to several structural and regulatory changes, CARE Ratings says, adding, "Private players underwent transformation leading to increased penetration, higher coverage, rise of multiple channels including agency, bancassurance, broking, direct and corporate agency, superior reach, and intensifying competitiveness in the market. The overall industry has also witnessed trends such as increased digital presence, emergence of InsureTech for innovations around customer education and service, products, technology and delivery systems for access."

LIC dominates with a three-fourth share in individual number of policies, while private players dominate with a two-third share in sum assured for individual policies.

In terms of number of policies, LIC continues to have a higher share at 75.9% in FY20 compared with 73.0% in FY10, which peaked at 84.4% in FY14, when compared to 24.1% share of private insurers in FY20. During FY20, life insurers issued total 288.9 lakh new individual policies, out of which LIC issued 218.9 lakh policies and private life insurers issued 69.5 lakh policies.

"While the private sector achieved a CAGR growth of (-) 6.4% (FY10-FY20) in the number of new policies issued against the previous year, LIC achieved a CAGR growth of (-)5.1% (FY10-FY20). This can be attributed to insurance companies has been more in the insurance premium (value) compared to the quantum of the policies sold annually (volume)," the ratings agency says.

The market share of private insurers in total sum assured for individual first year premium has been improved to 67.7% in FY20 as compared to 61.9% in FY18, while LIC’s share declined to 32.4% in FY20 as compared to 38.1% in FY18.

"The insurance business is expected to witness muted growth in the first quarter of FY21 due to COVID-19 and subsequent extended lock down, however protection plans could witness an increase due to rising awareness and the online channel could see robust growth," CARE Ratings concludes.

Source: Moneylife News & Views